You’ve pulled your credit report and score. You’ve compared credit card offers. You know exactly what you’re looking for.

It’s exciting to receive a credit card approval, but there’s something you need to know: you don’t necessarily have to accept the offer.

Before you say “yes” and begin to use your new credit card, there are some unique questions you’ll want to ask the issuer. Here are five to start with:

1. Do you report account information to all three major credit bureaus?

This isn’t something you typically have to worry about, but don’t take it for granted. Asking this question will put your mind at ease, as you’ll know once and for all if your activity is reported.

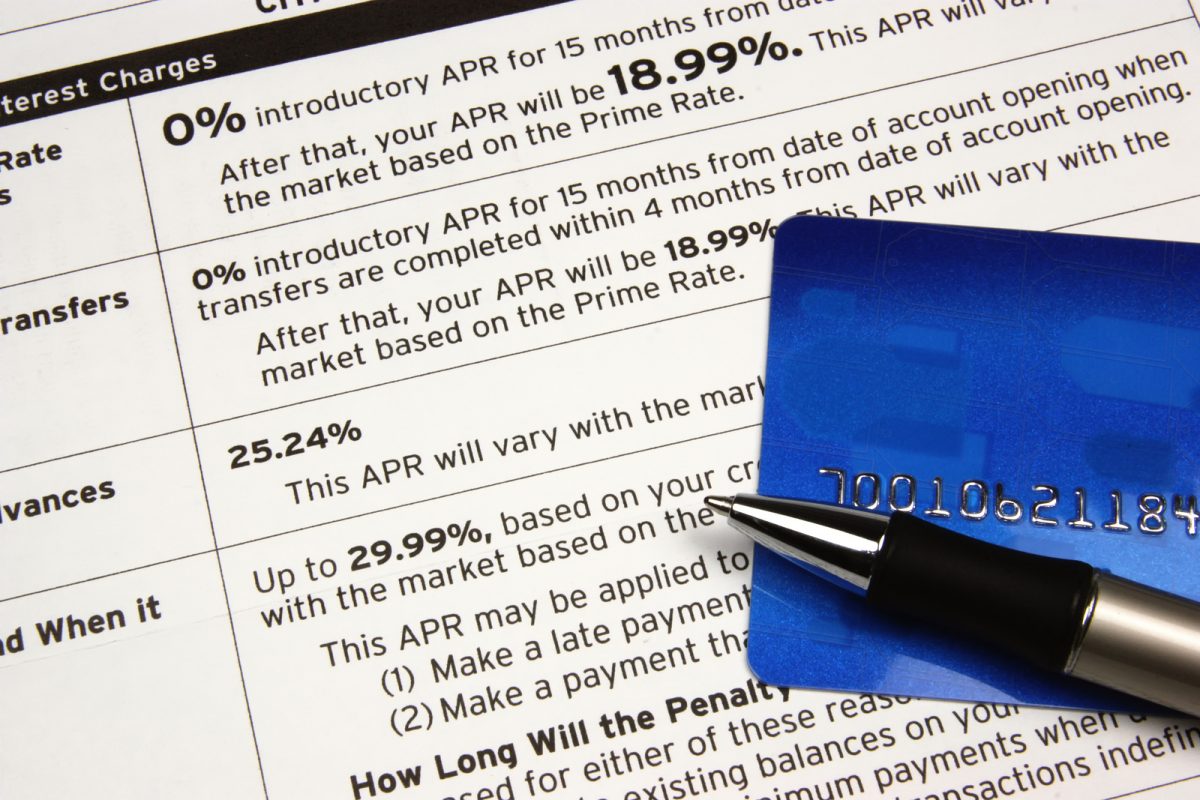

2. What happens if I make a late payment?

You have no intention of doing this, but you never know what the future could bring.

Maybe you run into an unexpected financial difficulty. Or maybe you’re traveling for work and simply forget to make your payment on time.

Piggybacking off this general question, here are two others to ask:

- What is the late payment fee?

- Will you forgive a late payment?

The credit card issuer will have a definitive answer to the first question. However, the second one is typically tackled on a case-by-case basis.

3. Will I have a variable or fixed interest rate?

Don’t ignore this question because you intend to pay your balance in full each month. There are times when this may not happen, so you need to understand the finer details of your interest rate.

In addition to knowing your current interest rate, request more information on whether it’s variable or fixed.

4. Can I select my own payment due date?

Most credit card issuers have no problem with this, so make sure you ask before you activate your card.

Even if they’re unable to change your due date for the first cycle, they should be able to submit a request for this to take place in the near future.

5. Are there any restrictions associated with the rewards program?

This only comes into play if you’ve applied for a rewards credit card, but it’s an important question to ask.

For instance, some credit card rewards programs have blackout dates, meaning you may not be able to use your points to travel when you want.

If there are too many restrictions, you may decide to opt against the offer and open your search up once again.

Final Thoughts

If you didn’t answer these questions when comparing credit card offers, be sure to do so before accepting the terms and conditions.

The most efficient way to collect information is by contacting the credit card issuer via live chat or phone. From there, you’ll gain access to a person who is willing and able to answer all your questions.

What do you think of these five questions? Would you add any others to the list?

What is my balance and how much credit do I need to pay for the month? 😉